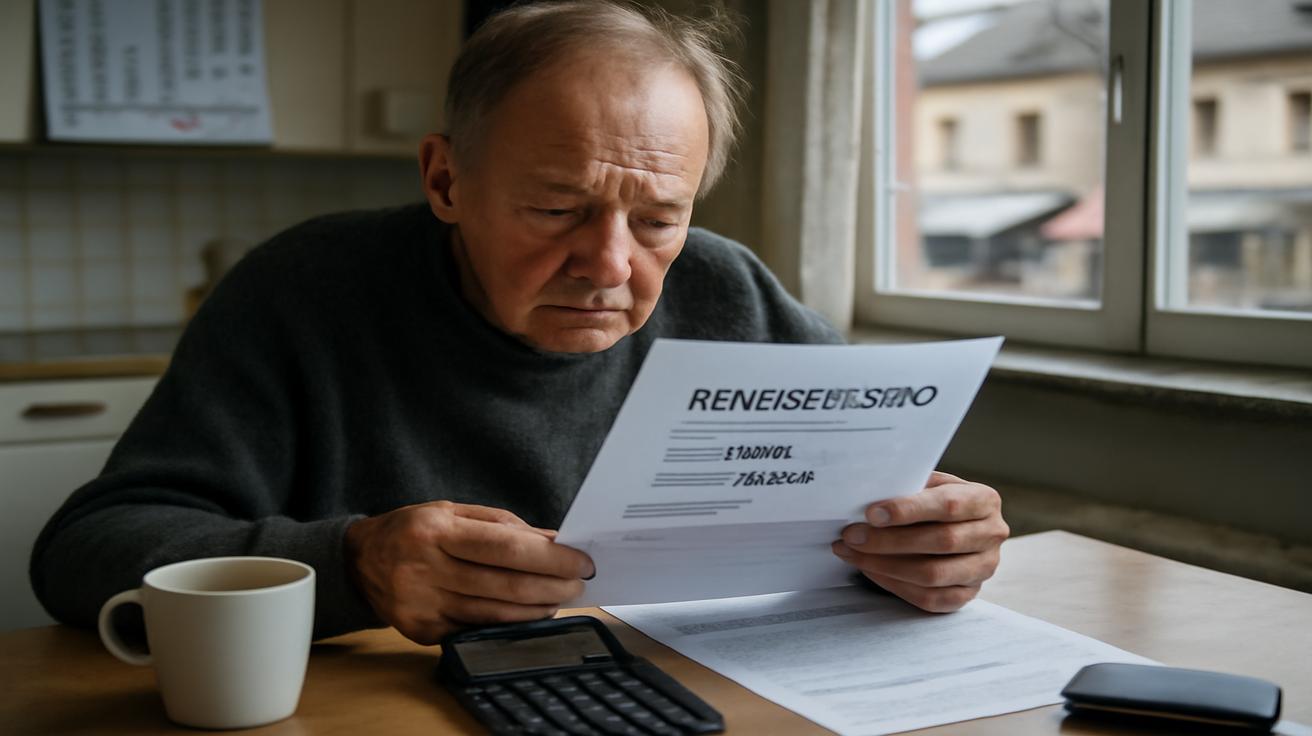

The letter lay on the doormat like any other: a pale rectangle among the supermarket flyers and the free local newspaper. Eva almost stepped over it on her way to put the kettle on. Outside, February light slid along the windowsill, thin and wintry, the kind that makes you pull your cardigan a little tighter even inside. She picked up the envelope, saw the familiar logo of the pension authority, and felt that small, almost automatic flutter in her chest. Not fear exactly, but a restless curiosity mixed with the quiet hope that, surely, the numbers would still add up.

She slit the top with a butter knife, steam from the just-boiled water fogging her glasses. The kitchen smelled of coffee and toast. Somewhere in the next building, a radio played an old song she half remembered from her twenties. She unfolded the paper and scanned the lines, looking for the part that mattered most: the amount for 2026. For a heartbeat, her brain did its usual trick—trying to make sense of the numbers, reading them as if nothing had changed.

Then she saw it. A smudge of absence. A little less than last year. Not much at a glance—just a handful of euros each month. But as she traced the difference with her finger, month by month, the total drifted down toward a number that felt bigger, heavier: almost €340 less over the whole year.

She exhaled sharply. The house felt suddenly quieter, every tick of the clock loud and separate. The kettle clicked off behind her. Out the window, a pigeon strutted along the roof tiles, indifferent to her small private loss. A silent loss—neatly printed in black and white, effective from January 2026.

The slow, quiet shrink of a pension

Loss doesn’t always arrive with drama. Often it slips in quietly, hidden in decimals and percentage points and three-line letters that use words like “adjustment” and “indexation.” The year 2026 is shaping up to be one of those slow-motion moments—no headlines screaming crisis, no sirens in the street, just millions of pensioners opening their mail and discovering that the numbers they’d built their peace of mind on have quietly shifted downward.

On paper, it might look small: a few euros a month, maybe twenty here, fifteen there. After all, who feels a single raindrop on their hand? Yet add them together over twelve months, and suddenly the figure has bones and weight. Up to €340 missing over the course of a year. That’s the winter heating bill. Three visits to the dentist. A train ticket to visit the grandkids. A week’s worth of groceries—more than once.

Economists talk about pensions in curves and charts. They speak of demographic pressure, contribution ratios, replacement rates. But for the people actually living on those pensions, the language is simpler and more physical—what goes in the fridge, whether the thermostat moves from 18 to 20 degrees, whether the new shoes can wait another season. The “silent loss” of 2026 is not just a technical adjustment; it’s a faint tightening of thousands of invisible belts.

And it’s happening in a way that’s dangerously easy to overlook, because it’s not arriving with a bang. It’s arriving with a shrug.

The mechanics behind the missing euros

To understand how a pension can shrink while nobody is really looking, you have to step briefly into the calm, slightly dusty world of formulas and policy rules. Don’t worry—we’ll come back to kitchens and real lives in a moment. But first, imagine your pension as a river.

For decades, while you were working, you poured water into that river: each paycheck sending a thin stream of contributions flowing forward in time. Governments and pension funds promised that, one day, the river would flow back to you—steady, dependable, enough to drink from with some security.

What many retirees don’t always see is that the amount of water flowing back is constantly being readjusted by a long list of invisible hands:

- Indexation formulas that decide whether your pension follows prices, wages, or a blend of both.

- Life expectancy calculations that whisper: “People are living longer, so the same pot must stretch further.”

- Inflation adjustments that sometimes lag behind the real price of bread, energy, and rent.

- Policy decisions, often framed as “technical corrections,” that shave off a little here, add a little there.

For 2026, several of these hands are moving at once. Perhaps indexation is being throttled back because of previous years’ high inflation. Maybe a rule that once promised full inflation protection is being applied with a cap. Or a temporary bonus that cushioned recent price spikes is quietly expiring. Individually, each measure sounds manageable, almost benign. Combined, they turn into that missing €340.

And all the while, another figure lurks in the background: inflation itself. Even if the nominal pension amount stayed exactly the same, the rising cost of daily life is already nibbling at its edges. When your pension is actually reduced—or simply not raised enough to match those prices—you’re hit with a double erosion: the number on the paper shrinks while the supermarket bill grows.

The household view: when €20 a month really matters

Policy papers like to speak in annual totals—€340 less in a year. But people live month to month, bill by bill, Monday to Sunday. Break that figure down, and it becomes easier to see how small numerical changes become tangible choices.

| Change in Monthly Pension | Yearly Difference | What That Can Mean in Daily Life |

|---|---|---|

| – €10 per month | – €120 per year | A month of basic mobile and internet costs, or two trips to the hairdresser |

| – €20 per month | – €240 per year | A winter coat plus shoes, or part of an annual heating bill |

| – €28–30 per month | ≈ – €340 per year | Several supermarket trips, a train ticket to see family, or a series of medical co-payments |

Numbers become real only when they meet the rhythm of a life. For some, a €30 monthly loss might simply mean choosing cheaper brands at the supermarket or delaying a planned purchase. For others living on the edge, it can slide directly into starker territory: skipping fresh fruit some weeks, turning the heating down one more notch, quietly withdrawing from social activities that now feel like luxuries.

And there is something particularly draining about a loss that earns no recognition. No one sends you a letter saying, “We know this will be hard; here’s why we’re doing it.” Instead, you receive glossy brochures talking about “sustainability” and “future resilience,” while your own resilience gets tested in the supermarket aisle.

It’s not just about comfort. It’s about dignity. The feeling that after decades of work, the deal you thought you had is being reworded in fine print, line by line.

The emotional weather of money

Money is rarely just money, especially in older age. It carries weather with it—personal microclimates of memory, fear, relief, and pride. A pension statement isn’t only a list of digits; it’s a reflection of an entire working life, condensed into a single monthly figure.

For someone like Eva, that figure is the echo of early mornings in the factory, of raising children between shifts, of staying late when colleagues called in sick. It’s the proof that the years stacked up to something solid. When that number begins to wobble or shrink, it can feel less like a technical correction and more like a question: Was it really enough? Did I do something wrong? Did I misunderstand the promise?

Psychologists talk about “threat perception” and “loss aversion,” the idea that we feel loss more intensely than gain. A €20 loss hurts more than a €20 gain delights. When you’re retired, with fewer ways to replace what vanishes, that effect intensifies. It’s not just the lost euros—it’s the sense of vulnerability they reveal.

Some pensioners respond by becoming almost forensic with their money: keeping every receipt, scrutinizing every bank statement, learning the code of tariffs and bonus rates. Others turn away, overwhelmed, preferring not to look too closely and hoping that, somehow, it will balance out. Neither reaction is irrational; both are different attempts to manage a creeping sense of uncertainty.

And then there is the silence. Many people will never tell their children or friends that their pension has dropped. Pride keeps the conversation light, even as calculations in the background grow darker. Social life becomes measured: “No, you go ahead this time,” “I’m fine at home tonight,” “It’s a bit far for me to travel.” The €340 that vanishes from a yearly pension can carry with it unseen costs in connection and joy.

Reading the letters, reclaiming some control

There is, however, another side to this story—the part where people begin to read those letters differently. Where the dense paragraphs and cautious tone are no longer something to endure but something to dissect. Because while you cannot single-handedly rewrite national pension laws, you can often influence how those broad rules play out in your own life.

It starts with slowing down. When that envelope arrives, resist the urge to glance at the first number and tuck it away in a drawer. Sit down with a pen, maybe a magnifying glass if the print is unkind, and look for four things:

- The exact monthly amount you will receive in 2026, compared to 2025.

- The explanation—however buried—for why it changed: indexation, corrections, tax withholding, or the end of a temporary supplement.

- Your tax situation: sometimes the pension itself hasn’t fallen, but increased tax or social contributions shrink the net amount.

- Any deadlines to contest incorrect data, update information, or apply for complementary benefits.

Then, consider the other parts of your financial landscape that might quietly help absorb the shock:

- Are you entitled to housing support or energy allowances that you’ve never claimed?

- Could you adjust the timing of certain bills to better match when your pension arrives?

- Is there a small savings buffer that could be protected—or rebuilt—for unexpected expenses?

This is not about magical solutions. A €340 yearly loss will not be erased by careful paperwork alone. But understanding is a form of power, however modest. It changes the story from “my pension is somehow less” to “my pension is less because of this, and here’s what I can do in response.”

And there is another, more collective layer. When thousands of people understand where, exactly, the silent loss comes from, their voices carry differently in public debate. It’s harder for decision-makers to hide behind abstractions when those affected can point to specific rules and their concrete effects: “This indexation cap means I will heat my home less next winter.”

Preparing for 2026: the year of the small check-in

Perhaps the most humane way to think about 2026 is not as a year of sudden crisis, but as a year that demands a new habit: the small financial check-in. Think of it like a regular visit to the doctor, or the way you listen to your own body a little more attentively with age.

Over the coming months, three gentle but firm actions can make a real difference:

- Review your pension statements and expected 2026 payments. Even if they’re only projections now, they’re early weather warnings.

- Map your fixed expenses realistically. Not in ideal terms, but in actual bills: rent or mortgage, energy, food, insurance, medications, transport.

- Talk to someone you trust. A family member, a financial adviser, a social worker, or a community group. Not to complain—but to compare notes, share information, and spot options you might miss alone.

There is a quiet courage in doing this. It means looking directly at figures that may unsettle you, and yet refusing to be simply at their mercy. It’s making sure that if there is help available, you’ve at least knocked on the door.

And perhaps, just perhaps, it’s also the year you begin to ask new questions of the system itself. Questions like: why should pensions fail to keep pace with the cost of a dignified life? Why should the oldest shoulders carry the burden of “sustainability” more than others? These questions are political in the deepest sense—not party-political, but rooted in the way we decide what a fair society owes its elders.

Beyond the numbers: what we really owe each other

On a chilly evening in early spring, Eva sat with her friend Marta on a park bench, watching the late light spill through the bare branches. Children’s voices flew across the playground; a dog chased a ball with extravagant joy. They spoke, as friends of a certain age often do, in a gentle weaving of memories and current aches: a grandchild’s new job, a cousin’s operation, the rising price of electricity.

Eventually, the conversation drifted, almost reluctantly, toward money. Toward that letter on the doormat. Toward 2026.

“They say it’s just a bit,” Marta shrugged, her scarf pulled tight against the breeze. “But it’s never just a bit, is it?”

Eva nodded, looking down at her hands. Hands that had packed boxes, wiped noses, held onto bus rails, signed contracts she barely had time to read. “It’s not only the money,” she said after a while. “It’s the feeling that they can move the line, and we just have to adjust around it.”

Perhaps that is the heart of the silent loss looming for 2026: not only euros misplaced, but trust diluted. The understanding that a promise made decades ago is now being interpreted in new, narrower ways. That what was once a firm line—a pension that would at least hold its value—has become more like a guideline.

But stories like Eva’s, multiplied by thousands, also hold something else: a reminder of what pensions were meant to be in the first place. Not charity. Not a grudging allowance. But a recognition that the work of a lifetime deserves, in its later chapters, the basic security to live without constant calculation and fear.

As 2026 approaches and the letters are printed, sorted, and posted, the loss they carry will remain mostly silent. There will be no ticking countdown, no flashing red light when the €340 vanishes. It will slip between days, between bills, between small adjustments that most people outside those households will never see.

Whether that loss stays silent in the public conversation is another question entirely. Because silence is not only imposed; it’s also a choice. And it might be that the most important response to this quiet shrinkage is equally quiet, but steady: people comparing their letters, sharing their experiences, asking sharper questions, and refusing to treat a smaller pension as an inevitable law of nature.

We live in a world where so much is loud, fast, and urgent. Yet some of the most consequential changes arrive softly, in the post, on a pale piece of paper you almost step over on your way to the kettle. In those moments, taking the time to read, to understand, and to talk about what’s happening may be one of the most powerful, human things we can do.

FAQ: Pensions and the looming loss in 2026

Why might my pension be lower in 2026?

Your pension can decrease or grow more slowly because of changes in indexation rules, adjustments for life expectancy, higher tax or social contributions, or the end of temporary supplements introduced in previous years. Even if the gross amount is similar, the net payment may fall once all these factors are applied.

Is everyone affected by the same amount, like €340 per year?

No. “Up to €340 less over the year” is an illustration of the potential scale of loss. The actual impact depends on the size and type of your pension, your country’s specific rules, your tax situation, and any additional benefits you receive.

How can I find out exactly how much I will lose or gain?

Check your official pension statements and any projected payment schedules for 2026. Compare the monthly net amount to what you received in 2025. If anything is unclear, contact your pension provider or pension authority and ask for a detailed explanation of the differences.

What can I do if my pension drops and I’m struggling?

First, verify that your data is correct and that no errors have occurred. Then explore whether you’re eligible for housing assistance, energy support, social benefits, or local aid programs for low-income pensioners. Speaking with a social worker, financial adviser, or trusted family member can help you identify options you may not see alone.

Can I influence these pension changes at all?

You cannot usually change the formulas yourself, but you can join pensioners’ associations, participate in public consultations, contact elected representatives, and share your experience in community or media discussions. Collective, informed voices are more likely to shape future pension policy than isolated complaints.

Should I be worried about the long-term future of my pension?

It’s wise to be attentive rather than constantly anxious. Follow updates from your pension fund or authority, review your statements annually, and, if possible, maintain a small savings buffer. Staying informed and engaged gives you the best chance to adapt to changes and to push for fairer rules.

How often do such “silent losses” happen?

Pension adjustments—both upward and downward—are part of most modern systems. “Silent losses” tend to occur when pensions fail to keep pace with inflation or when policy tweaks gradually reduce real purchasing power. They may not make headlines every year, but over a decade they can add up significantly, which is why regular review and open discussion matter.